Mathematical Theory of Mills Ratios

Deep dive into the mathematics of tail thickness

2026-02-02

Source:vignettes/theory.qmd

Introduction

The Mills ratio, first tabulated by Mills (1926), provides a fundamental measure of tail thickness in probability distributions. This article explores the mathematical foundations and theoretical properties of Mills ratios.

Definition

The Mills ratio is defined as:

where: - is the probability density function - is the cumulative distribution function - is the survival function

Asymptotic Behavior

Normal Distribution

For the standard normal distribution, as :

The leading term dominates, indicating thin tails.

Show code

x <- seq(2, 10, by = 0.5)

mills_exact <- mills_ratio_normal(x)

mills_approx <- 1/x

data.frame(

x = x,

exact = mills_exact,

approximation = mills_approx,

relative_error = abs(mills_exact - mills_approx) / mills_exact

) x exact approximation relative_error

1 2.0 0.4213692 0.5000000 0.186607766

2 2.5 0.3542651 0.4000000 0.129097919

3 3.0 0.3045903 0.3333333 0.094366218

4 3.5 0.2665678 0.2857143 0.071826076

5 4.0 0.2366524 0.2500000 0.056401786

6 4.5 0.2125706 0.2222222 0.045404410

7 5.0 0.1928081 0.2000000 0.037300793

8 5.5 0.1763230 0.1818182 0.031165512

9 6.0 0.1623777 0.1666667 0.026413767

10 6.5 0.1504370 0.1538462 0.022661748

11 7.0 0.1401042 0.1428571 0.019649373

12 7.5 0.1310794 0.1333333 0.017195519

13 8.0 0.1231320 0.1250000 0.015171014

14 8.5 0.1160821 0.1176471 0.013481802

15 9.0 0.1097873 0.1111111 0.012058123

16 9.5 0.1041336 0.1052632 0.010847378

17 10.0 0.0990286 0.1000000 0.009809323Student’s t-Distribution

For the t-distribution with degrees of freedom, as :

This linear growth indicates fat tails.

Exponential Distribution

For the exponential distribution with rate :

The constant Mills ratio characterizes the exponential tail decay.

Inequalities and Bounds

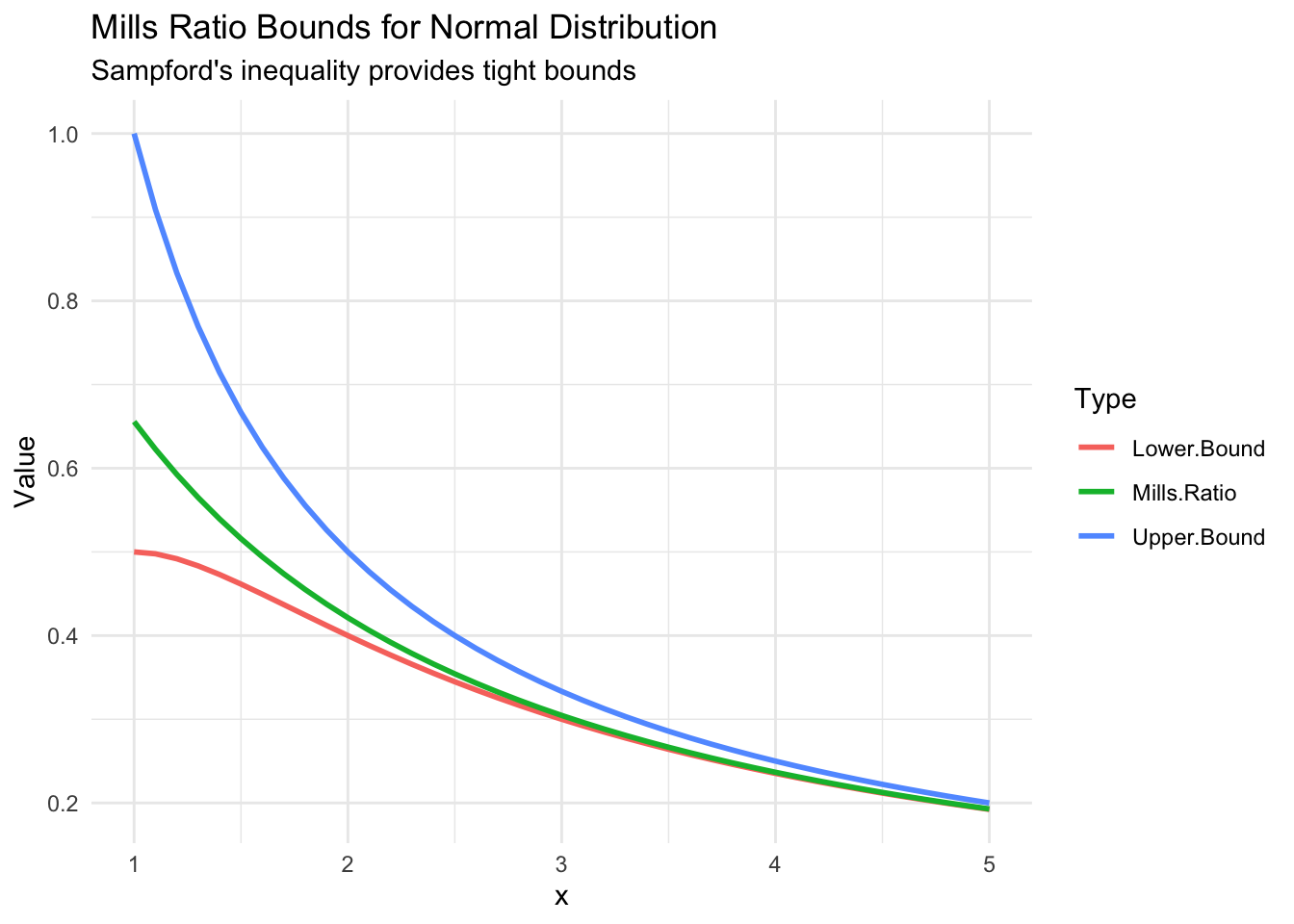

Sampford’s Inequality

Sampford (1953) established bounds for the normal Mills ratio:

These bounds become tighter as increases.

Show code

x <- seq(1, 5, by = 0.1)

mills <- mills_ratio_normal(x)

lower_bound <- 1/(x + 1/x)

upper_bound <- 1/x

plot_data <- data.frame(

x = x,

`Mills Ratio` = mills,

`Lower Bound` = lower_bound,

`Upper Bound` = upper_bound

) %>%

pivot_longer(-x, names_to = "Type", values_to = "Value")

ggplot(plot_data, aes(x, Value, color = Type)) +

geom_line(size = 1) +

labs(

title = "Mills Ratio Bounds for Normal Distribution",

subtitle = "Sampford's inequality provides tight bounds",

y = "Value"

) +

theme_minimal()Warning: Using `size` aesthetic for lines was deprecated in ggplot2 3.4.0.

ℹ Please use `linewidth` instead.

Relationship to Other Functions

Hazard Function

The hazard function (failure rate) is the reciprocal of the Mills ratio:

Error Function

For the normal distribution:

where is the complementary error function.

Tail Classification

Mills ratio behavior classifies tail thickness:

| Behavior | Tail Type | Example |

|---|---|---|

| Decreasing () | Thin | Normal |

| Constant () | Exponential | Exponential |

| Increasing () | Fat | Student’s t |

Applications in Statistics

Truncated Distributions

The mean of a truncated normal distribution above point is:

Extreme Value Theory

Mills ratios appear in the study of: - Order statistics - Record values - Peaks over threshold models

Computational Considerations

Numerical Stability

For large , direct computation can be unstable. Use:

Show code

# Unstable for large x

unstable_mills <- function(x) {

pnorm(x, lower.tail = FALSE) / dnorm(x)

}

# Stable using log scale

stable_mills <- function(x) {

exp(pnorm(x, lower.tail = FALSE, log.p = TRUE) - dnorm(x, log = TRUE))

}

# Compare at x = 10

x_test <- 10

c(unstable = unstable_mills(x_test),

stable = stable_mills(x_test),

package = mills_ratio_normal(x_test)) unstable stable package

0.0990286 0.0990286 0.0990286